Borrow now, pay later

Chester Water Authority says the city’s bankruptcy spooked lenders—but its refinancing cycle also left little room when conditions tightened.

Welcome back, readers! This Part Two of my look at how the management of a water authority is getting tangled up in Chester, Pennsylvania’s bankruptcy.

In the first issue, I described how a long-running legal fight over who controls the Chester Water Authority (CWA) has spilled into rate-setting and day-to-day costs for customers. Here, I’ll explain how over the past six years, the CWA’s capital improvement financing strategy became one of postponement—one that worked until it didn’t.

This edition runs long. Hopefully you’ll forgive me for not staying true to this newsletter’s title in favor of being precise with laying out the facts.

Avoiding the bill

For much of this year, CWA leadership focused on refinancing tens of millions in debt in order to avoid sharp rate hikes and spare customers from sticker shock. But in October, the authority announced a 14% rate increase would take effect in January 2026 anyway.

The CWA blamed the city and instability from the bankruptcy and takeover battle. But this year’s events are also just the latest chapter in CWA’s cycle of borrowing and refinancing to avoid a large rate increase for consumers, and now it’s stuck holding the bag.

Here’s the throughline: Since 2019, CWA relied on a series of private, shorter-term borrowings with large near-term maturities. Each refinancing bought time and avoided an immediate rate shock. But it also kept the next big payment right around the corner—so when litigation risk and operating pressures mounted, the cost of borrowing jumped and the rate increase became hard to avoid.

When I asked the CWA if repeated borrowing and increased debt also played a material role in narrowing its options this year, the authority cast the 2019-2025 borrowings as ones that kept options open: They “facilitated short call features for the CWA’s flexibility” and were “a function of its capital requirements for capital improvements, not to avoid ‘large balloon payments,’” CWA said in an email.

But this response is hard to square with the summary in the authority’s April 2025 refinancing resolution:

Instead, the CWA’s response focused largely on the fact that Chester’s bankruptcy exit plan includes the water authority as an asset and contemplates either selling or leasing it. This, CWA wrote, “created the specter of unquantifiable and unacceptable risk to potential traditional lenders regarding the CWA’s credit quality…and security.”

Fair enough, and I’ve documented the disturbing mismanagement of the city’s finances and its outdated governance that led to its bankruptcy. But what about the CWA’s own choices around debt structure and refinancing?

Here’s what the CWA’s own documents show via https://savecwa.org and the Municipal Securities Rulemaking Board’s public database).

Balloon payments and bad timing

The CWA’s last public borrowing was in 2014—a relatively conventional long-term debt issuance to support a growing regional water system’s capital improvements and system maintenance. But after that, several events made conventional borrowing more difficult.

In 2017: The private utility Aqua made an unsolicited bid to buy the Chester Water Authority. That offer triggered what has become a prolonged legal fight between the city and the CWA over who had the right to sell the system at all.

Importantly: This argument predates the city’s bankruptcy filing in 2021 and was led by the previous mayoral administration.

Bottom line: The sale fight introduced a new fiscal risk in the eyes of lenders and bond buyers who had to factor in the possibility that the authority could be sold, restructured, or subjected to new oversight. It didn’t create CWA’s financial challenges, but it did change how lenders viewed the authority.

In 2019: The CWA issued $28 million in bonds through a private placement to fund new capital projects.

Importantly: The authority wanted to finance $35 million, but the original lender backed out. The CWA said the city’s meddling and the sale uncertainty controversy were to blame.

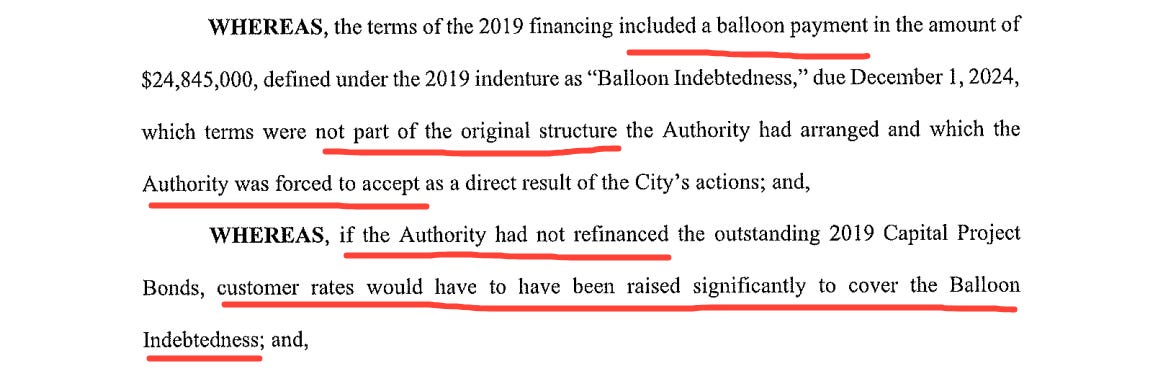

Bottom line: The authority accepted less-than-ideal terms—including a large balloon payment due in 2024. This may have reduced near-term costs but deferred a substantial obligation into the future.

In 2022: As the balloon date approached, the authority sought refinancing to avoid the large payment noting that if it didn’t, “customer rates would have to have been raised significantly to cover the Balloon Indebtedness.”

Importantly: The new, $43 million deal paid off the 2019 debt and funded additional capital work. It was also the first to occur after the city of Chester had entered into bankruptcy.

Bottom line: This private sale just put off the CWA’s large bill. It included a balloon payment due in 2026—even larger than the previous one.

In 2023: The CWA lost a major customer. This is referenced in Moody’s Investors Service’s eventual downgrade of the authority, though it did not identify the customer. Evidence suggests it was Aqua, which the authority told me stopped purchasing water at one of their connection points around that time.

In 2024: Moody’s notified the CWA it would review the 2022 bonds because Chester’s bankruptcy exit plan included potentially assuming CWA’s debt. This introduced a new risk for bondholders who had only considered that debt would be paid off or transferred to a private entity in the event of a sale.

This brings us to 2025. In April, the CWA board authorized another new borrowing/refinancing—this time for up to $60 million. Once again it was framed as the responsible way to manage debt while avoiding sudden, extreme rate hikes and to cover ongoing capital needs.

Note: the authority still raised rates during this period—just not by a lot. Disclosures show that in 2022, 2023, and 2024, it raised rates by 5%, 5% and 8%, respectively.

Moody’s one-notch downgrade came in June. It cited two reasons:

A “decline in debt service coverage and liquidity” due to the decline in business from a “major wholesale customer.” Rebuilding its cash position “will require several years of rate increases.”

The uncertainty over control of the CWA (which the state Supreme Court has yet to rule on) which “could have dramatic consequences for the authority’s rating,” Moody’s said. “The longer this litigation drags on, the greater the risk CWA faces from potential market access limitations and other challenges relating to this controversy. The most drastic scenario would be one in which the City of Chester assumes the authority’s debt, even temporarily. In that event, the rating on the authority’s bonds could be downgraded many notches.”

Now the CWA had two bad choices: Find the cash for its balloon payment or borrow again under even worse circumstances.

The CWA told me it pursued multiple options: regional traditional lenders, governmental lenders, tried to get bond insurance (it was denied) and tried to negotiate an extension on the 2022 bonds. “Traditional lenders simply had no interest in assuming the risk of the City’s pursued actions,” it wrote. “Following the exhausting of other alternatives, CWA was required to pursue lending from a lender specializing in distressed credits.” Recent filings with the MSRB indicate the refinancing and borrowing deal was executed in two tranches at rates of 7% and 11%.

Though the authority’s rate hike resolution framed the decision as one caused entirely by the city, in its statement to me the CWA said its planned rate increase “in part addressed the debt service coverage and liquidity issues raised by Moody’s.”

Who really pays

Bond downgrades don’t change what an issuer pays for existing debt, but it does impact the cost of future debt. Because the CWA’s playbook had become one where the next borrowing date was always looming on the horizon, the downgrade had an instant impact on the CWA’s debt costs.

What this adds up to is less a story about villains than about compounding risk. CWA had real infrastructure needs and faces legitimate uncertainty from litigation and Chester’s bankruptcy plan. But its financing strategy also made the authority unusually dependent on being able to refinance—again and again—on reasonable terms. When borrowing costs spiked, the cushion disappeared, and the rate increase became the release valve.

In a PUC-regulated system, those trade-offs would play out in a public rate case with standardized disclosures. For a municipal authority, they play out through board decisions, bond markets, and—eventually—customers’ bills.

That’s why the fight over control matters. Not because one side is right and the other is wrong, but because when financial risk builds quietly over years, transparency and governance are the main checks before the bill comes due.