The most debt-burdened states

The fifth one may be a surprise.

Happy Finance Friday, readers! Greetings from The Rabbit Hole, where I have spent way too much time playing around with charts using data from a new Fitch Ratings report on state-long term liabilities. Below, I’ll review the report’s takeaways and share my own observations from the data. (This is a chart-filled post, so it’s best viewed on a computer or tablet. All charts are built by me using Fitch’s data.)

Easy come, easy go

The “market exuberance” during the pandemic recovery propelled a 24% rise in state pension asset portfolios, said Fitch, but the resulting “decline in liability burdens appears to be short-lived.” Some of those gains in 2022 have already been erased and preliminary data show assets falling an average of 5.2% in fiscal 2023.

On the plus side, many states used some of their surplus revenue in 2022 to make extra deposits into their pension plans. Those supplemental deposits totaled almost $9 billion, with California and Connecticut contributing an extra $2.3 billion and $4.1 billion, respectively, under budgetary mechanisms predating the pandemic. Additional excess deposits were made by Washington, Indiana, Kentucky, and New Jersey.

After playing with the data, I have a few thoughts of my own:

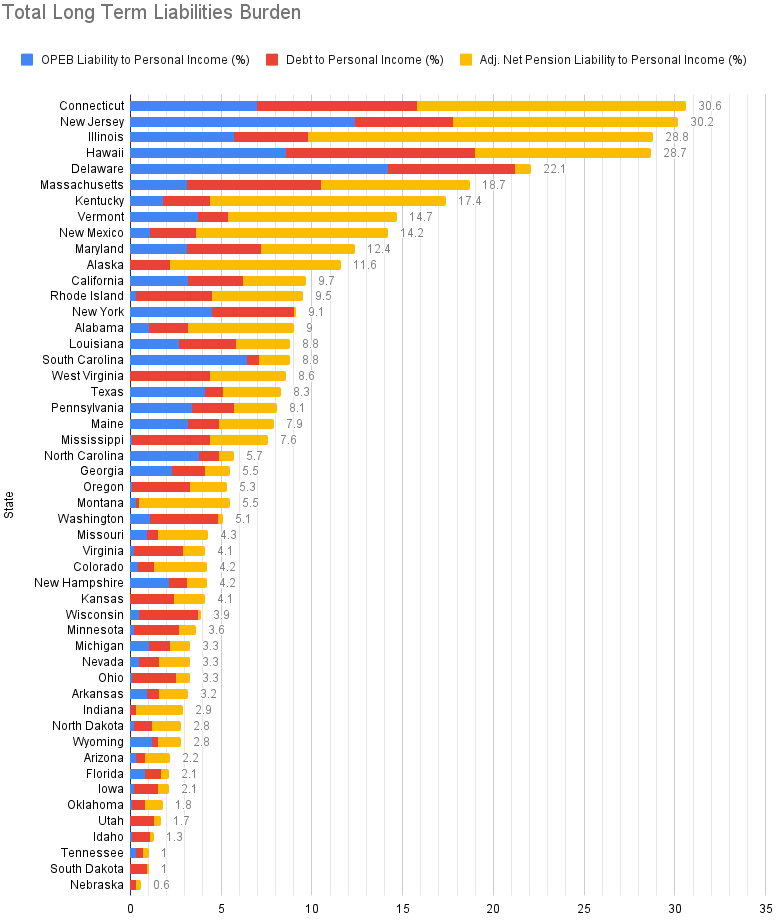

Five states’ total long-term liabilities are equal to at least one-fifth of personal income.

Retiree healthcare represents the largest debt burden in 11 states.

The way ratings agencies standardize liability data has implications for the impending Financial Data Transparency Act.

States with the most burdensome debt

Fitch’s report looked at unfunded state pension liabilities, retiree healthcare liabilities (OPEB) and outstanding debt (typically bond debt). The data requires a couple explanations:

States don’t all use the same math to value their pensions, so ratings agencies use their own standard to determine the value of all state unfunded liabilities. This “adjusted net pension liability,” or ANPL, typically increases the liability (see graph further down) but it provides a more uniform picture across the states.

Fitch also presents these liabilities as a percentage of state personal income. State personal income usually mirrors a state’s economy and is a good measure of a state’s taxing power and ability to pay for government services.

OK, with that out of the way, the top five most indebted states in terms of economic burden are: Connecticut, New Jersey, Illinois, Hawaii and Delaware. Here’s the full chart.

Delaware being near the top of this list was a bit of a surprise to me but, as you can see, that’s because of its high retiree healthcare burden (more on that below). Other notes about the top five:

Kentucky and New Jersey have seen the sharpest improvement since fiscal 2016, largely due to policy changes that prioritize making full pension payments. Kentucky’s liability burden dropped by 8 percentage points and New Jersey’s dropped 7 points.

Illinois and Connecticut only had small improvements.

Hawaii’s burden worsened by 1.6 percentage points.

Retirement obligations in the highest-ranking states also include local school district employees, which increases the total liability. This isn’t the case in most of the least-burdened states.

Where retiree healthcare is a bigger burden than pensions

Nearly a dozen states have a bigger issue with OPEB liabilities than pensions:

Keep reading with a 7-day free trial

Subscribe to Long Story Short to keep reading this post and get 7 days of free access to the full post archives.